Revive Therapeutics (TSXV: RVV) (RVVTF) Looks Significant Undervalued

Valuing small and micro-cap biopharma companies is a difficult task. Most have no revenues, let alone earnings where valuation multiples can be applied. And even when revenues or earnings do exist, the market can be fickle on what specific multiples to apply. Discounted cash flow seems to be the tool of choice for many professional investors, but that too is highly subjective and at the mercy of inputs like discount rates, terminal values, and predicting peak sales.

There is one truth however that investors can generally feel comfortable applying when looking at the valuation of small and micro-cap biopharma companies. That is, the later the stage of development the more valuable the asset. Though not a perfect linear equation, a company with a Phase 3 drug in development will likely be valued higher than a company with a Phase 2 drug, or Phase 1 drug, etc. Additionally, the size of the market and the existing competition plays an important role in valuation as well. Again, nothing is an exact science, but the larger the market and the fewer the competitors, the better.

I’ve been spending a lot of time lately looking at rare diseases. While they may not be terribly large markets, often there is minimal competition and room for aggressive pricing. Orphan drug designation and the potential for things like Priority Review and Fast Track status also help to increase the valuation of small and micro-cap biopharma stocks.

Clinical Development – Why Later Is Almost Always Better

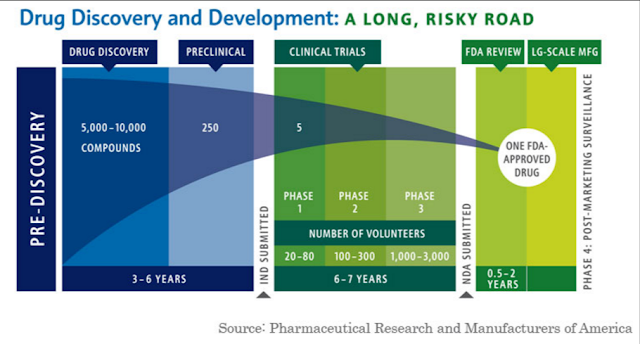

Later is better is a pretty simple concept when it comes to biopharma investing. I know the average BioNap reader understands this concept, so I will not bore you with too many details. The graphic below sums up the reason why rather nicely. It shows that for every one drug that gets approved, potentially as many as 10,000 get weeded out during clinical and preclinical testing. That means, generally speaking, the further a drug progresses the better chance it has to get to the market.

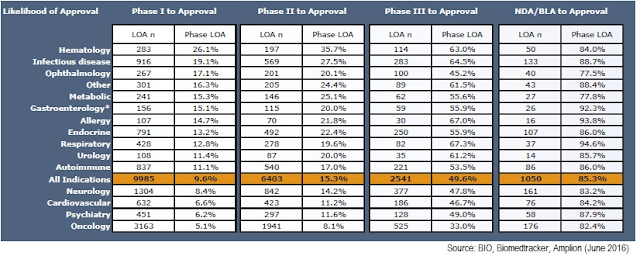

For example, work done by BIO, Biomedtracker, and Amplion published in June 2016 shows that the odds of approval increase for every clinical trial completed (see below). As such, investors will then clearly place more value on assets as they move through the various stages of clinical development. And, each preclinical or clinical program that a biopharma company successfully completes with a drug candidate, generally speaking, is a step to a higher valuation.

This type of analysis helps take a little bit of the guesswork out of the equation when looking to value biopharma companies. In this regard, one way to look at the valuation of a specific small or micro-cap biopharma company might be on a relative basis with a peer group of companies with similar stage drugs in development that target similar sized markets.

Revive Therapeutics – A Quick Background

Revive Therapeutics (TSXV: RVV) (RVVTF) is one such company that looks vastly under-valued based on this type of analysis. Revive is developing bucillamine, a dithiol derivative of tiopronin for the treatment of cystinuria. Cystinuria is a rare autosomal recessive genetic disorder characterized by an impairment of transport of the dibasic amino acids, cystine, ornithine, lysine, and arginine (COLA) in the kidneys; the important clinical manifestation of which is a build-up of cystine in the urine, which in turn results in crystallization and stone formation in the kidneys and bladder. No curative treatment of cystinuria exists, and typically patients have a lifelong risk of stone formation, repeated surgery, and impaired renal function.

In the U.S., about one of out every 15,000 individuals has cystinuria, which equates to a target population of approximately 21,000 individuals (1). For patients that cannot reduce stone formation on conservative programs such as increased fluid intake and alkali therapy, pharmaceutical intervention is recommended. This is about 5,000 patients in the U.S. each year. This qualifies as an ultra-rare orphan disease.

The two leading pharmaceutical products for the treatment of cystinuria are Retrophin’s Thiola® (tiopronin) and Valeant’s Cuprimine® (d-penicillamine). d-penicillamine is the first-line therapy, but use is limited due to serious side effects, including serious blood disorders such as aplastic anemia and agranulocytosis, kidney damage, Goodpasture’s syndrome, myasthenia gravis, liver damage, and allergic skin reactions (pemphigus). The incidence of adverse events ranges between 30 and 60% (2). Cuprimine is also used to treat Wilson’s disease, an autosomal recessive genetic disorder of hepatic copper metabolism. Valeant sold roughly $75 million worth of Cuprimine in 2015 for both indications.

Tiopronin received U.S. FDA approval in 1988 for the prevention of cystine stone formation in patients with severe homozygous cystinuria with urinary cystine greater than 500 mg/day, who are resistant to treatment with conservative measures of high fluid intake, alkali and diet modification, or who have adverse reactions to penicillamine. The product was available as a generic and largely unpromoted until the rights to Thiola® were acquired by Retrophin, Inc. in May 2014 (3). Retrophin subsequently raised the price of the drug some 20-fold (4) and currently controls the bulk of the U.S. market.

Thiola® costs roughly $27 per 100mg pill (5), and with the majority of patients taking 1,000 mg per day (6), the yearly cost of the drug is roughly $100,000. Estimated net sales of Thiola® to Retrophin in 2015 were $55 million (average of available reports). Evaluatepharma estimates that Thiola® will post sales of $100 million in the U.S. in 2017 and has peak sales of $200-250 million. I estimate the total U.S. market for cystinuria products is approximately $500 million.

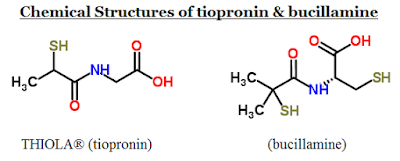

Tiopronin has similar efficacy and mechanism of action to d-penicillamine. Tiopronin is an active reducing agent which undergoes thiol-disulfide exchange with cystine to form a mixed disulfide of tiopronin-cysteine. The drug is ideal for patients with allergic reactions or intolerability to penicillamine and considered to be the most tolerable of the two drugs (7). Retrophin has also greatly improved patient access and support for the drug since taking over in 2014. Investors can see the chemical structures of tiopronin and bucillamine below, noting the thiol (-SH) groups.

Revive believes that bucillamine can offer patients a safer, more effective treatment option than tiopronin or d-penicillamine. Theoretically, bucillamine should be twice as effective as Thiola® at the same concentration or equally as effective at lower concentrations, potentially making the drug more tolerable to patients.

Bucillamine has been used in Japan and Korea for decades, with the majority of the use in rheumatoid arthritis. Researchers have conducted in vitro and in vivo (n=3) studies demonstrating theoretical proof-of-concept for bucillamine in the treatment of cystinuria (8). Bucillamine received U.S. FDA Orphan Drug designation for the treatment of cystinuria in November 2015 (9). This will protect the drug from generic competition for 7-years post approval, along with tax incentives and the potential for expedited approval.

– Next Steps For Revive

Revive is currently planning to initiate a Phase 2 clinical study with bucillamine (n=30) at up to ten centers in the U.S. The estimated cost of the study is $1.5 million and management estimates the total study will take approximately six months to complete enrollment, with top-line data to follow shortly thereafter. Revive recently completed a raise of $2.34 million (10, 11), so the company has enough cash to advance bucillamine in this program.

Following the presentation of the data, I expect that Revive will sign a development and commercialization agreement for bucillamine as a treatment for cystinuria. Obvious interested parties include Valeant and Retrophin, although given the potential superior pharmacology of bucillamine to Thiola® and the Orphan Drug designation, I believe that Revive will have ample opportunity to shop the drug around and sign the best deal for shareholders.

What’s Revive Worth?

Revive has what looks to be a safe and effective drug for cystinuria, an estimated $500 million opportunity in the U.S. The bucillamine mechanism of action is similar to that of two proven drugs in the market, tiopronin and d-penicillamine, with in vitro data showing a potential 40-50% increase in efficacy at the same concentration. Bucillamine has been used safely for over three decades in Japan and Korea. The planned U.S. Phase 2 trial in 30 patients should confirm these findings when the data read-out mid-2017.

The next obvious question is, what’s this all worth? What is a biopharma company worth with a Phase 2 drug for an ultra-rare orphan disease that targets a $500 million potential market?

– The Traditional Approach

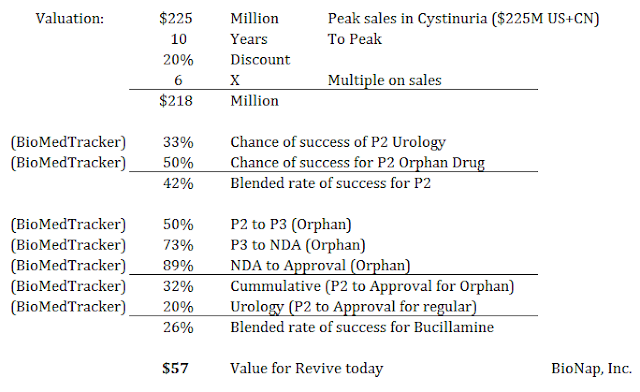

The traditional approach to valuing Revive is to forecast sales of bucillamine in cystinuria and then apply some sort of probability-adjusted NPV. According to EvaluatePharma, Thiola should do around $100 million in sales in 2017 and peak between $200 and $250 million. The total market opportunity in the U.S. for bucillamine and tiopronin is approximately $500 million. I believe that 30-40% market share for bucillamine is very realistic, so peak sales for the drug in cystinuria are likely in the $150 to $200 million range. I also believe that, if approved, bucillamine will see $50 million in sales off-label for rheumatoid arthritis, which is the drug’s primary use in Japan and Korea, and potentially as much as $25 to $50 million in Wilson’s disease. This places my best-guess peak sales for the drug at $225 million.

I expect the U.S. Phase 3 trial will start in 2017 and complete in 2018. I expect Revive to file for approval in 2019 and launch in 2020. I think the drug will peak six years after approval and that orphan drug protection will expire in 2027. The U.S. specialty pharmaceutical industry currently trades with a price to sales ratio of 6x (12) and Revive likely has a cost-of-capital near 20%.

According to BIO, BiomedTracker, and Amplion, a Phase 2 urology asset should progress to commercialization 20% of the time (see table above). However, drugs for rare orphan diseases succeed at far higher rates than chronic of high prevalence diseases. In fact, a Phase 2 orphan disease drug succeeds roughly 32% of the time, based on the historic data compiled by BIO, Biomedtracker, and Amplion (13). Plugging all these inputs into an equation, traditional valuation analysis pegs the fair value of Revive Therapeutics today at $57 million. That’s a seven-fold increase from today.

– Peer Valuation Approach

– Peer Valuation Approach

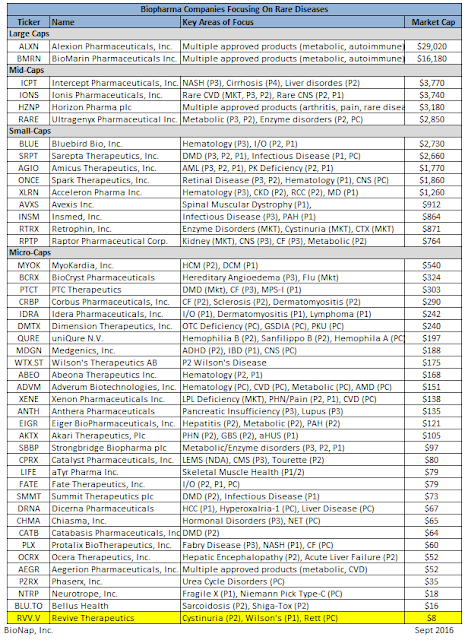

Another way to look at the valuation of Revive today is to compare the name to other biopharma companies that focus on the treatment of rare diseases. Below I have compiled a list, albeit certainly not all-inclusive, of various biopharma companies that have programs for rare or orphan diseases. Revive’s valuation today at only $8 million is striking, all the way at the bottom of this group.

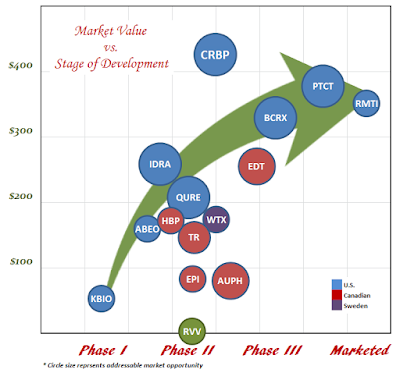

I’ve also created a scatter plot showing the relative valuation of Revive, a company with a drug currently approved in Japan and Korea and in Phase 2 in the U.S. for a rare disease, compared with other small biopharma companies with Phase 2 and Phase 3 drugs that target rare diseases. The plot is fairly straightforward, graphing stage of development vs. market value, with the size of the circle representing the size of the market for the disease. Canadian companies are shown in red.

Investors can see once again that Revive’s valuation, nearly off the bottom of the chart, simply does not match up with bucillamine’s stage of development or market potential. For example, Wilson Therapeutics (WTX.ST) is a Swedish-based biopharma company developing a drug in Phase 2 for Wilson’s disease. Wilson Therapeutics has a market value of $175 million. Revive’s Phase 2 drug for Cystinuria targets a larger market and is far less risky than Wilson’s Decuprate®. And, Revive expects to move into Phase 2 with bucillamine for Wilson’s disease in earl 2017.

ESSA Pharma (EPI.TO) is a fellow Canadian biopharma company developing EPI-506 for prostate cancer. The drug is in Phase 2 and requires achievement of far more rigorous clinical endpoints that bucillamine in cystinuria. ESSA trades with a market value of $95 million.

Corbus Pharmaceuticals (CRBP) has one drug in clinical development called Resunab undergoing three Phase 2 trials for orphan conditions. These include cystic fibrosis, systemic sclerosis, and dermatomyositis. Corbus has limited clinical data with Resunab in these indications. Phase 1 data shows the drug to be safe with an attractive pharmacokinetic profile, but the clinical development program is far more risky that bucillamine. Corbus trades with a market value of over $300 million.

Helix Biopharma (HBP.TO) is another fellow Canadian company that trades with a market value of $165 million. The lead candidate is a topical interferon Alpha-2b for the treatment of certain skin/mucosal lesions caused by HPV infections. The market is roughly the same size as the cystinuria market, albeit far more competitive with several big pharma competitors.

I would suspect, simply based on the stage of development, the risk of development, and the potential peak market opportunity for the drug, Revive should be trading with a market value in excess of $100 million.

Upcoming Events

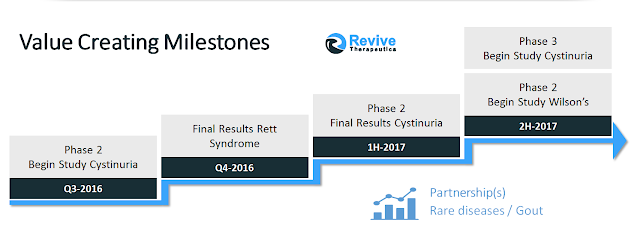

Below is a slide from the company’s investor presentation that highlights some upcoming events that may help close the valuation gap between Revive and its peer-group.

Conclusion

It’s not an easy task to try to come up with an accurate fair value for Revive Therapeutics. As such, I cannot say with exact certainty what Revive shares are worth today. The scatter plot analysis is far from an exact science. The traditional NPV analysis based on projecting peak sales is also far from an exact science. I’ve even model built a discounted cash flow (DCF) model for bucillamine in cystinuria (not shown), and even that also shows a fair value far in excess of today’s price. So although I cannot say exactly what Revive shares are worth, I’m confident they are worth more than what they trade for today.