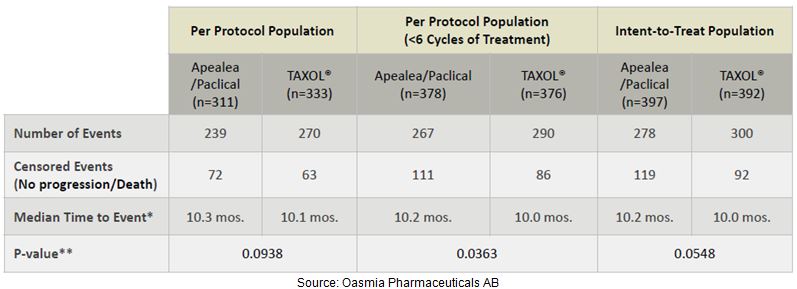

Oasmia Pharmaceuticals (NASDAQ: OASM) is firing on all cylinders. Earlier this week, the company announced positive overall survival (OS) data from its Phase 3 clinical study with Paclical/Apealea® for the treatment of ovarian cancer. After completing six treatment cycles, patients on Paclical/Apealea® plus carboplatin had a median overall survival of 25.7 months compared to 24.8 months for patients that had received Taxol® (paclitaxel) plus carboplatin. The data are consistent with the previously reported progression-free survival (PFS) data presented at ASCO in May 2015. The PFS data demonstrated that Paclical/Apealea® was non-inferior to paclitaxel when used in combination with carboplatin, 10.2 months vs. 10.0 months, respectively.

{kind=link}

Positive Overall Survival In Ovarian Cancer

The Phase 3 study (NCT00989131) was an open-label, randomized, multicenter study conducted in 789 patients with recurrent epithelian ovarian cancer. With positive OS data now in hand, Oasmia plans to file for U.S. FDA approval of Paclical® around the end of 2016. Paclical® was approved in Russia and the Commonwealth of Independent States (CIS) in April 2015 and Oasmia shipped the first batch of product to its Russian distribution partner, Pharmasyntez, in December 2015. Oasmia filed for approval of Apealea® in the European Union in February 2016.

I see tremendous potential for Paclical/Apealea® in the treatment of ovarian cancer. Visiongain estimates that the market for ovarian cancer drugs will reach $1.7 billion by 2019. Ovarian cancer is the fifth leading cause of cancer death in women, and approximately 22,280 new cases will be diagnosed in 2016. The National Cancer Institute, through its Surveillance, Epidemiology, and End Results (SEER) program, estimated over 185,000 women were living with ovarian cancer in the U.S in 2011. The five-year survival rate for ovarian cancer is 45.6%. Data from the European Cancer Observatory notes 44,149 diagnosed cases of ovarian cancer in Europe in 2012.

Standard of care for ovarian cancer is paclitaxel or docetaxel plus carboplatin, with paclitaxel regimens holding approximately 70% share. With U.S. FDA approval, Oasmia has the potential to move Paclical® into first-line therapy. The product has been granted Orphan Drug designation in both the U.S. and EU for this indication. There are clinical studies and case reports that indicate that Celgene’s Abraxane® (nab-paclitaxel) is used off-label by oncologists to treat certain types of epithelial ovarian cancer. However, it is difficult to quantify what percent of the approximate $1.15 billion in global Abraxane® sales are coming from ovarian cancer use, as Celgene does not comment on the off-label use of the drug.

A Nice Market Opportunity

Paclical/Apealea® in epithelial ovarian cancer easily looks like a $300 million opportunity. I base that number of a modest 20% penetration with the drug into the generic paclitaxel market, assuming Paclical/Apealea® is priced at a slight discount across the board to Abraxane®. Upside to the Paclical/Apealea® sales number stems from follow-on indications, including breast cancer, an indication for which Oasmia is currently conducting Phase 1 clinical trials.

Although I suspect that Oasmia may choose to license Paclical® to a commercial partner in the U.S., based on conversations with management, the company believes it could successfully market and sell the product themselves, especially in select regions around Europe. Targeting breast cancer as the second indication is interesting because, if approved, Oasmia would have two indications for Paclical/Apealea® both targeting women. The strategy makes an interesting niche for promotion. And if successful, the company only further strengthens the case for a potential take-out, which was exactly the Abraxis BioScience strategy with Abraxane® between 2005 and 2010 prior to the $2.9 billion buyout by Celgene.

A Platform For Success

Oasmia is now looking to duplicate the success it has with Paclical/Apealea® by expanding its pipeline using the company’s proprietary XR-17 platform technology. XR-17 is designed to improve solubility, facilitate administration, enhance the pharmacological profile and bioavailability, and allow for dual encapsulation of water-soluble and water-insoluble APIs in one nanoparticle. According to a 2014 report, an estimated 70% of molecules in clinical developmental and 40% of approved drugs are believed to be poorly soluble.

{kind=link}

Beyond Paclical®, Oasmia has two additional clinical stage candidates, Doxophos®, an XR-17-doxorubicin formulation and Docecal®, an XR-17-docetaxel formulation. Oasmia estimates the market for Doxophos® exceeds $600 million on a global basis. The company has already filed for approval of Doxophos® in Russia and expects to gain market authorization by the end of 2016. The market opportunity with Docecal® is significantly larger, perhaps even twice the size of Paclical®. Sanofi’s Taxotere® achieved peak sales of $2.8 billion in 2010, nearly twice the size of Bristol’s Taxol® (paclitaxel). On March 30, 2016, Oasmia announced the first patient enrolled in the company’s Phase 1 clinical study with Docecal®.

Management is also working on a dual cytostatic agent delivered as one infusion. The unique properties of XR-17 make this combination possible, where multiple active substances can be bound in one micelle, even if the two substances differ in water solubility. Pre-clinical studies with OAS-19, the code name for the company’s XR-17 dual cytostatic agent, have shown promising results. I think this could be a tremendous product for Oasmia. Keep in mind, the standard of care for ovarian cancer is a combination taxane (paclitaxel or docetaxel) and platinum-based (cisplatin or carboplatin) chemotherapy. These agents are given as two separate infusions. Combining, for example, docetaxel and carboplatin into one infusion could greatly improve compliance, tolerability, and patient outcomes.

An excellent example of this type of strategy is the recent success of Celator Pharmaceuticals (NASDAQ: CPXX) with Vyxeos®. Vyxeos® is a nano-scale co-formulation of cytarabine and daunorubicin in one liposomal injection. The current standard of care for acute myeloid leukemia (AML) is separate injections of cytarabine and daunorubicin. With Vyxeos®, Celator has been able to demonstrate an improvement in overall survival and a reduction in healthcare burden. This combination essentially makes prescribing Vyxeos® over the previous standard as a “no-brainer”. I think this is exactly where Oasmia is heading with OAS-19.

Veterinary Medicine Division Provides Meaningful Upside

Beyond Oasmia’s efforts with Paclical/Apealea®, Doxophos®, Docecal®, and OAS-19, the company has a growing animal health division lead by a U.S. FDA approved product, Paccal-Vet®. Paccal-Vet® is the first injectable chemotherapeutic agent authorized for the treatment of squamous cell carcinoma and mammary carcinoma in dogs. Oasmia received conditional approval by the U.S. FDA for Paccal-Vet® under the Minor Use and Minor Species (MUMS) designation in the U.S., a designation similar to orphan designation for humans, in February 2014.

Management believes the company will be allowed to market Paccal-Vet® for up to five years while the company collects the remaining required effectiveness data for full approval. Oasmia is eligible for incentives to support the full approval to conduct this additional work. The company is currently planning additional efficacy studies in dogs to collect all the necessary efficacy data for full U.S. approval of Paccal-Vet® for mammary carcinoma and squamous cell carcinoma.

According to the American Pet Products Association (APPA), between the U.S. and Europe, there are 143 million dogs and 160 million cats registered by pet owners in these regions. An astonishing 78% of these animals take prescription medication! It’s a $30 billion market between the U.S. and EU. According to the Center for Cancer Research and CanineCancer.com, approximately six million dogs in the U.S. are diagnosed with cancer each year, of which approximately one-third have cutaneous disease. There have been no nanoparticle formulations of injectable chemotherapeutic agents formulated specifically for dogs or cats before Paccal-Vet®. Abraxane® is ineligible for use in animals because it contains human albumin, thus making the market wide-open for Oasmia’s improved formulation.

Oasmia previously licensed Paccal-Vet® to Abbott Anima Health, a division of Abbott Labs. However, in February 2015, Abbott sold its animal health division to Zoetis, Inc. Zoetis subsequently returned the rights of Paccal-Vet® back to Oasmia following a significant restructuring of its business in June 2015. Zoetis and Oasmia approximate the size of the cancer chemotherapy market for dogs in the U.S. at $500 million. Veterinarians tend not to use generic paclitaxel in dogs due to the animals’ severe reaction to the Cremaphor El excipient. Paccal-Vet® will be the only paclitaxel-product available for animal use by Veterinarians. The opportunity to Oasmia looks to be in the $50 to $100 million range, with upside to this number as Oasmia works to expand the label to include mast cell tumors or additional indications. Doxophos-Vet®, a doxorubicin formulation for lymphoma in dogs, is currently in Phase 2 clinical trials.

Conclusion

Oasmia has several things going for it that I like. Firstly, this is a proven business model validated by Celgene’s $2.9 billion acquisition of Abraxis in 2010 and Sorrento’s sale of Cynviloq®, a nanoparticle micellar paclitaxel solution to NantPharma for up to $1.3 billion in 2015. Oasmia’s market capitalization is only $165 million, and the company looks to be traveling down the same path as Abraxis.

Secondly, I like that there seems to be low clinical risk. The Phase 3 trial with Paclical/Apealea® is complete, with the product demonstrating non-inferior PFS and OS to Taxol®. The product is already on the market in Russia, under review in the EU, and will be under review in the U.S. by the end of the year. The clinical risk with Doxophos® and Docecal® look equally manageable.

Thirdly, I like the fact that Paclical® is already on the market and generating revenues in Russia. Yes, the Russian pharmaceutical market is not nearly the size of the U.S. or European market, but the approval of Paclical® in Russia shows that Oasmia management can execute by getting its drugs approved and striking a commercial partnership to monetize the asset.

Fourthly, I like the potential expansion of the pipeline, both with new indications for Paclical® and with Doxophos® and Docecal®. Oasmia clearly has a strategy in place to create value for shareholders, and they are building upon existing success with a validated model. As I noted above, I’m very intrigued by OAS-19, a combination agent in early-stage trials, based on the recent success of Celator’s Vyxeos® in AML.

Finally, I like the fact that the company has an animal health division with FDA approved Paccal-Vet®. There have been no nanoparticle formulations of injectable chemotherapeutic agents formulated specifically for dogs or cats before Paccal-Vet®. The opportunity is Oasmia’s to capture.

Oasmia looks to be following a similar path to Abraxis and Celator. These positive attributes, along with the low market valuation, leads me to believe the positive momentum in the stock should continue.