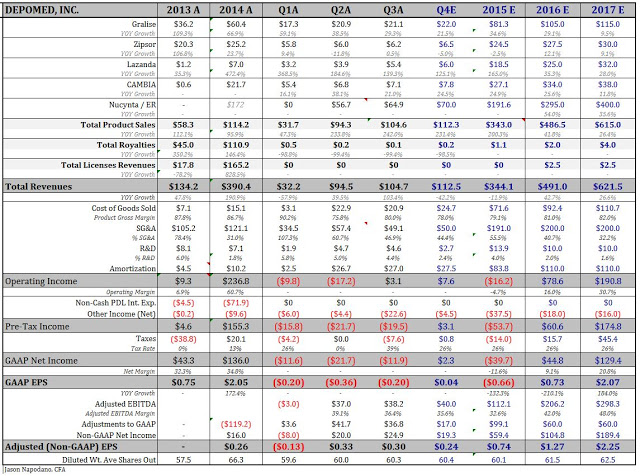

I’m long Depomed (DEPO). Here is my model:

Depomed has now raised guidance two quarters in a row (Q2, Q3). I think the current guidance is still conservative. Management is guiding to revenues between $336 million and $348 million for 2015. I model $344 million, with most of the growth coming from Nucynta / ER. Upside to my numbers comes from re-acceleration in products like Gralise, Cambia, or Zipsor on a piggy-backing effect of the increased sales force and promotional efforts around Nucynta / ER.

Management think Nucynta / ER will do $500 million in sales in 2018. These seems reasonable to me. I do not model out to 2018 yet, but for 2017 I see the current trajectory yielding sales of $400 million (+36% from 2016) and $500 million would be an achievable 25% growth over 2017. I do not think Nucynta / ER ever gets to “blockbuster” status (> $1 billion), but for a company the size of Depomed, that’s not excessenal for success. Ultimately, I think the franchise peaks out around $700-800 million in sales, spinning off around 50% operating profits at peak.

Let’s look at the valuation.

For 2016, I think revenues will be $491M. If we apply a simple 4X revenue multiple on our 2016 number, we arrive at approximately $2.0 billion in market cap. With 61 million shares basic outstanding, that equates to $33 per share. Even 3X revenues still gets the stock to $24 per share and the historic range for specialty pharma is between 3x and 5x. Yes, we are at the low-end of the range right now due to the misadventures of companies like Valeant and Horizon, but if you are a long-term buyer then the bottom of the cycle is the perfect entry.

For 2016, I think they will report adjusted EBITDA of $206M. If we apply a simple 10X on our Adjusted EBITDA number, we arrive at a market cap of $2.1 billion. We need to back out the $500M in net debt that the company anticipates having by the middle of the year (note management said they plan to pay off $100 million in the Q2-2016), so we are looking at a market cap of $1.6 billion, or around $26 per share. Historic range on EV/EBITDA is between 12-15X. In the “bio-bubble” times earlier this year, Depomed and peers were selling at 14-15X. Again, if you’re a long-term buyer of these types of stocks, you want to establish a position now, and hopefully ride both multiple expansion and metric growth over the next 2-3 years. That’s how the pros do it.

For 2016, I think adjusted EPS (note I’m using non-GAAP numbers to back-out significant non-cash items such as amortization and non-operating items such as interest expense and transaction costs) will be $1.27 per share. Please note, for EPS I am using the fully-diluted number of approximately 85 million shares. I argue a P/E of 15X is rather low for Depomed, a company projected to revenues 42% and earnings 95% in 2016. Nevertheless, using 15X EPS gets us to $19 per share. Using 20X EPS, still 0.5x growth, gets us to $25 per share.

So there you have it, using three common valuation techniques, the stock looks fairly-valued between $24 and $33 per share. My target is $28 per share, which happens to be a nice middle-ground based on these various exercises and consistent with my discounted cash flow (DCF) model (not shown).

Early over the summer I argued that Horizon (HZNP) needed to pay $35 per share to complete the merger. I still believe this. After all, if I think $28 per share is fair, then why sell for fair. If you are going to sell, sell for an offer that cannot be refused. By the way, the current offer from Horizon equates to only $17.50 per share, which is a joke and has about as much a chance of closing as John Blutarsky’s GPA.

In conclusion, I still think this is among the best management teams in the business and I still think numbers are conservative. The stock is cheap and fundamentals are strong. That’s the ideal combination for a core-holding.