Last week, Gilead Sciences entered into a global partnership for the development and commercialization of filgotinib, a JAK1-selective inhibitor for inflammatory conditions, with Galapagos NV. Galapagos will receive an upfront payment of $725 million consisting of a cash license fee of $300 million and a $425 million equity investment. In addition, Galapagos is eligible for payments up to $1.35 billion in milestones, with tiered royalties starting at 20% and a profit split in co-promotion territories. This is a great deal for Galapagos shareholders.

Investors have bene waiting for cash-rich Gilead, a company that exited the third quarter 2015 with $25.1 billion in cash and securities in the bank, to do a deal, and this deal with Galapagos looks like just the beginning of what could be a major shopping-spread for the biotech behemoth in 2016. Although Gilead has little commercial experience in inflammatory diseases such as rheumatoid arthritis and Crohn’s disease, the proven mechanism of action of JAK inhibitors and the comparable data on filgotinib to other treatments in the class was too attractive for Gilead to pass up.

Although not quite as big as the acquisition of Receptos by fellow behemoth Celgene for $7.2 billion in July 2015, the deal above represents a growing interest by the industry’s bigger players looking for new treatment options to some of the largest pharmaceutical markets. Orphan drugs are all-the-rave in small-cap biotech right now, but there’s always room in the pipeline for a potential blockbuster, and Gilead thinks filgotinib can compete for market share in the $40 billion global immuno-inflammatory market.

I spent some time looking at filgotinib, mostly comparing the drug to Lilly/Incyte’s Phase 3 baricitinib and Pfizer’s Xeljanz® (tofacitinib), both JAK inhibitors of sorts, specifically looking at the data in rheumatoid arthritis (RA). What I found is that apples-to-apples comparisons are difficult given the different designs and patient populations of each study, but something else struck me as interesting the more I delved into the data. Can-Fite’s piclidenoson (formerly CF101), a drug that most biotech investors know very little about, compares pretty well to these drugs universally believed to be blockbusters.

Piclidenoson – What You Need To Know

Can-Fite is developing piclidenoson for the treatment of psoriasis and rheumatoid arthritis (RA). For the purpose of this analysis, we will focus primarily on RA and how the drug compares to the JAK inhibitors. For my deep delve into the opportunity in psoriasis, please see my article from August 2015.

Piclidenoson is an orally bioavailable A3 adenosine receptor (A3AR) agonist. Scientists have discovered that the Gi protein-associated cell surface receptor A3AR is overexpressed in both inflammatory and cancer cells vs. low expression of the receptor if found in normal cells (1). The mechanism of action of adenosine agonism in inflammatory conditions involves the inhibition of the formation of cAMP and its downstream effectors, PKA and protein kinase B/Akt (PKB/Akt). The reduction in the activity of these two kinases results in the deregulation of the Wnt and the nuclear factor kappa-B (NF-κB) signal transduction pathways, leading to the inhibition of tumor necrosis factor α (TNF-α), interleukin-6 and -12, macrophage inflammatory proteins and receptor activator of NF-κB ligand (RANKL) (2, 3).

As such, Can-Fite believes A3AR may serve as a target for pharmacological intervention in inflammatory states, such as psoriasis or rheumatoid arthritis. More importantly, no safety issues related to toxicology have been reported thus far from studying piclidenoson in mice, rats, and dogs. Phase 1 clinical testing in humans showed linear pharmacokinetic parameters in doses up to 10 mg. Single oral doses up to 5 mg and repeated doses up to 4 mg every 12 hours have been safe and well tolerated.

Piclidenoson in Rheumatoid Arthritis

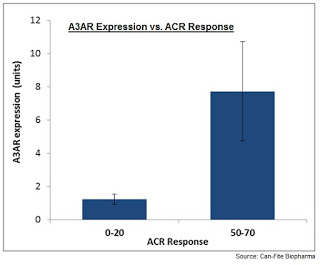

Phase 2a clinical testing with piclidenoson in RA was published in the Journal of Rheumatology in 2008. The primary goal of this early-stage study was to assess the clinical activity and safety of the drug, but also get a sense on whether or not expression level of A3AR was directly correlated with patient responses. If so, this suggests utilization of A3AR expression as a biomarker for the pharmacodynamic and therapeutic effects of the drug. Results showed a strong response on the ACR scale, a measure of percent improvement in RA disease symptoms, and that there was a correlation between A3AR and response to the drug (4).

Over the next several years, Can-Fite conducted several more Phase 2 programs, some positive and some not-so-positive, looking to characterize the efficacy of the drug with respect to ACR scores and the response to A3AR expression. Specifically, the company has demonstrated that oral therapy with piclidenoson results in reduced expression of A3AR and moderation of symptoms in patients with RA as a monotherapy, but not in combination with the anti-inflammatory agent methotrexate (MTX). This is likely due to the fact that patients pre-treated with MTX already demonstrate A3AR down-regulation thereby diminishing piclidenoson treatment effect.

The most recent Phase 2b study (NCT01034306) was a multicenter, randomized, double-blind, placebo-controlled study comparing 1 mg piclidenoson to placebo. The primary endpoint of the study was ACR20 after 12 weeks of treatment. Importantly, patients were enrolled into the study based on A3AR expression level, defined as 1.5-fold over a predetermined normal population standard. Seventy percent of screened patients were found to have high levels of A3AR. A total of 79 patients were randomized into the trial with 71 (90%) completing the 12 weeks of treatment.

Results show a statistically significant difference in ACR20 between piclidenoson and placebo (49% vs. 25%, p = 0.04). ACR50 (19% vs. 9%) and ACR70 (11% vs. 3%) responses were not significant, but both favored the piclidenoson arm. Interestingly, in a subpopulation of treatment-naïve patients, with no prior systemic therapy, the response to piclidenoson was much higher compared to the response of the whole population, with ACR20 of 75% and ACR50 of 50%.

Piclidenoson vs. The JAKs

Piclidenoson vs. The JAKs

To put the piclidenoson Phase 2b data above into context, below I’ve created a table that shows the data from all four Phase 3 studies with baricitinib, a drug that Wall Street believes will post sales of $720 million in 2019 for Eli Lilly (5). For reference, data from Lilly’s RA-BEAM study included an active comparator arm of AbbVie’s Humira® (adalimumab), a drug that posted global sales of $12.5 billion in 2014 in numerous indications, including RA and psoriasis.

The baricitinib data looks very good. It is not hard to see why most analysts believe this drug will be a blockbuster for Lilly. However, Lilly acquired baricitinib well before any of the Phase 3 programs read-out. The deal struck between Lilly and Incyte back in December 2009 included $90 million upfront, $665 million in potential milestones, and tiered double-digit royalties on global sales up to 20%. Deals have certainly gotten more expensive since 2009, but this was a fairly nice deal at the time for Incyte, and looks like a ‘Home Run’ for Lilly based on the data above.

Last week, Gilead acquired filgotinib from Galapagos for $300 million upfront, $425 million equity investment, and the potential for $1.35 billion in milestones, with tiered royalties starting at 20% and a profit split in co-promotion territories. Filgotinib has potential in Crohn’s Disease (CD), so we cannot directly attribute all the payments to the potential in RA, but even if the value is split evenly among the two indications, that’s still a sizable increase in value compared to what Lilly scooped-up baricitinib for exactly six years early. The Phase 2 data for filgotinib is presented below, and although impressive, is slightly less robust than the baricitinib data.

Of course, both these drugs will be battling for market share among the JAK inhibitor prescribing rheumatologists with Pfizer’s Xeljanz® (tofacitinib), already FDA-approved and on the market. Xeljanz® generated $127 million in global sales in the third quarter 2015, and is likely to post sales in 2016 in excess of $700 million. Wall Street analysts are projecting sales in 2020 of $1.6 billion, due largely to the expected approval of the drug in psoriasis in 2016 or 2017. Xeljanz® data in RA is presented below.

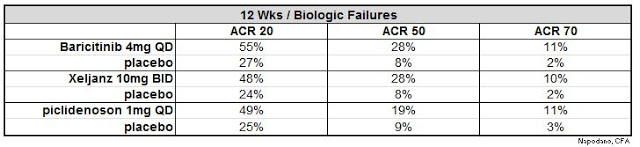

I’ve hit you guys with a lot of data above. To simplify, I’ve tried to pull out the specific data above that compares most closely on a patient population to Can-Fite’s Phase 2b data with piclidenoson. More specifically, data at 12 weeks in moderate-to-severe patients with RA that are biologic-failures. This data is presented below.

To make it even easier to view, I’ve put the above data into a graph, with the red bars on each column representing the placebo patients.

Several things immediately jump out. Firstly, the placebo patients in all three trials performed remarkably the same, meaning the patient populations were likely very similar at baseline. Secondly, the ACR20 and ACR70 data for piclidenoson are nearly identical to Pfizer’s Xeljanz® and statistically non-inferior to Lilly’s baricitinib. The ACR50 data on piclidenoson is numerically lower than Xeljanz® and baricitinib, and could either speak to the potential A3AR responder analysis or simply just be the results of only having data from 71 patients in the smaller Phase 2b program.

For previously untreated patients, Can-Fite’s published data shows an ACR20 score of 75% at 12 weeks. This compared well with Lilly’s Phase 3 data from RA-BEGIN, which shows baricitinib ACR20 at 12 weeks of 79% vs. methotrexate (MTX) monotherapy at 59%. The 50% score on ACR50 for piclidenoson also compared quite well with baricitinib at 55% and methotrexate at 33%.

Time To Show Some Love For Can-Fite

Time To Show Some Love For Can-Fite

I’m baffled by the low valuation for Can-Fite (CANF) shares. The market capitalization of Can-Fite is only $43 million, and roughly $20 million of that is cash. Piclidenoson, which should enter Phase 3 trials on a global basis during the first half of 2016, has data as good as filgotinib in RA and Gilead just shelled out $725 million for the drug last week. As I’ve written in the past, the Phase 2 data with piclidenoson in psoriasis is as good, if not better than Celgene’s Otezla®, a drug that Wall Street believes will post sales near $1 billion in 2016 (7).

Although Lilly’s barcitinib looks like the lead horse in this race, the potential to pre-select patients for piclidenoson based on A3AR biomarker expression will certainly be interesting to many patients and physicians, especially in the first-line setting. The data above suggests that piclidenoson is superior to methotrexate (MTX), the most common first-line therapy for treatment-naive patients with advanced RA (8), with a similar mechanism of action in down-regulation of A3AR and comparable safety and tolerability.

Once the company initiates the Phase 3 RA study with piclidenoson in 2016, it will be interesting to see if investors start to pay attention to the story. Pfizer, Lilly, Celgene, and Gilead have made their bets in this market, but there are still plenty of major players that might be interested in piclidenoson, a drug that could likely replace MTX in the first-line, treatment-naive setting in patients with high A3AR expression. That is certainly intriguing for Can-Fite shareholders because it seems like these deals just keep getting bigger and bigger.

Related:

– Read about Can-Fite’s CF102 for hepatocellular carcinoma (HCC), currently in Phase 2 with data expected mid-2016, and the company’s new preclinical data with CF102 in NASH.

– Read about RedHill Biopharma (RDHL) RHB-104, currently in Phase 3 for Crohn’s disease.